My aim for this guide is to introduce you to Bitcoin Mining, give you an overview of how mining supports the Bitcoin ecosystem, show you ways you can create Bitcoin through a process called Mining and make money at the same time.

What is Bitcoin and the Blockchain?

You have probably found this guide knowing exactly what Bitcoin is, if so skip to the next section. However if the word “Bitcoin” is new to you I recommend you also read my guide “Demystifying Cryptocurrencies”.

Bitcoin is a Cryptocurrency technology based on computer software (think of a recipe) and an alternative to our traditional monetary system. It is digital in format and enables buyers and sellers to trade directly with each other using a software application called a “Wallet” on on computers and smartphones.

Unlike money, Bitcoin does not require humans and infrastructure like a “centralised” bank to manage your account, validate transactions and hold everything inside a financial ledger. Instead the Bitcoin software automatically manages the financial ledger consisting of accounts (called “Wallets”) and all transactions ever made in a decentralised fashion distributed across thousands of computers (called Nodes) worldwide.

All transactions are stored in containers called “blocks” which are sequentially linked to the previous block of transactions making a chain called the “Blockchain”. Each block of transactions confirms the integrity of the previous block making it impossible to fake transactions or commit fraud. Key to Bitcoin’s nature is its security and the person who owns the Bitcoin does not reveal their name, address or any personal details, instead they have a “public key” which references their Bitcoin account (Wallet) on the Blockchain and a “Private key” which only they know which is used to authorise transactions.

As well as Bitcoin being a currency it can be traded and exchanged for traditional money which can make owning it profitable depending on market conditions.

What is Bitcoin mining?

The decentralised Bitcoin blockchain ledger holds a record of all transactions that have ever taken place and the balances of people’s Bitcoin Wallets. This system needs the computational power of the nodes on the network to follow the software, keep the ledger updated and validate transactions in a secure manner. The nodes doing this work are called “Bitcoin Miners”.

What are Bitcoin Miners?

Bitcoin miners are computers with vast processing power and unlike your average desktop computer are designed specifically to process millions of transactions per second to support the Bitcoin network. Throughout this guide I will be referring to the Bitmain AntMiner S9j which is the current industry standard Bitcoin mining machine used by companies and individuals to mine Bitcoin worldwide.

How do Miners maintain the Bitcoin Network?

The Bitcoin ledger is maintained by miners on the network who relay the changes (transactions made by buyers and sellers and individual Wallet balances) encrypted (scrambled) and anonymously between each other. There are thousands of Bitcoin miners carrying out this service currently and the idea behind having so many miners maintaining the network means that if one goes down it doesn’t stop or affect the efficiency of the Bitcoin network (in fact since Bitcoin’s inception in 2009, the network has never stopped). This is much more efficient when you compare it to the Visa or Mastercard network which banks rely on for maintaining transactions and have been known to crash in recent years.

How are Bitcoin transactions are validated?

Miner’s use their immense computational power to compete with other Miners on the Bitcoin network to find a transaction to validate. They are actually solving a cryptographic maths problem and once solved it validates the transaction. Miners are essentially processing trillions of numbers per second to do this which uses a lot of electricity.

Built into the Bitcoin software is a set of rules that have to be followed for a transaction to be validated. These include making sure the transaction is not double spent (the buyer pays twice) and that a person’s Bitcoin Wallet has sufficient funds to pay for the transaction. This is all done automatically by the miners following the Bitcoin software.

Once a transaction is validated this is announced to the network automatically and the other miners stop trying to validate that transaction and all move onto compete for the next transaction to solve.

How do Miners make money?

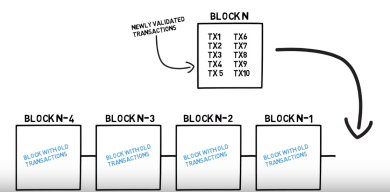

The Bitcoin Blockchain consists of blocks containing transactions joined together in sequential order (see diagram of blocks 1 to 4). Each block gets filled with transactions and the maximum size for a block is 2mb (1000 typed pages). As soon as a miner fills a block with transactions they have validated they receive a amount of Bitcoin as a reward.

This concept is called “Proof of work” because the miners have to prove they have done something in order to get the reward.

The standard transaction fee which the buyer pays today is approximately 0.0001 Bitcoin and on average there could be 300 to 1000 transactions per block, so between 0.03 and 0.1 Bitcoin can be rewarded to the miner for creating a block. On average a block can be created in under 10 minutes. At the time of writing this guide, one Bitcoin is worth $6500 dollars making the reward for creating a block anywhere between $195 and $650 – imagine if Bitcoin doubled in value and you are a miner!

Can Miners create Bitcoin without validating transactions?

As well as validating transactions miners use their power to follow the Bitcoin software and create Bitcoin blocks. The same conditions apply in that once a block is created they receive a reward.

How Miners work together using Pools

It is extremely difficult for one miner to work on its own to validate transactions and create blocks so it can receive a reward in Bitcoin. That’s why mining pools are created which allow multiple miners to join their processing power and work together so they can do the mining together a lot quicker.and share the reward.

How secure is mining Bitcoin?

The Bitcoin blockchain isn’t controlled by any one person or company. There are over 8000 computer nodes running the bitcoin ledger and all have to agree and come to consensus for the blockchain to work. If a miner where to falsify a transaction all the other nodes on the network would have to agree for it to be a valid transaction. Below are a few examples showing how secure the Bitcoin ledger is:

Can a Miner falsify a Transaction?

Each block also includes a piece of information from the previous block in the blockchain. If a miner added or modified a transaction to an older block they would not only have to re-solve the old block, they would have to re-solve all blocks between that block and the current block. Plus all the other nodes would not recognize the re-solved blocks unless anyway.

The miner in questions would need an extremely large amount of processing to do this operation and would have to do the solving faster than all the other nodes on the network combined.

Could someone take control of the Bitcoin blockchain?

The only way for someone to sabotage Bitcoin would be to control 51% of all the nodes. Then they would have to change the Bitcoin ledger on all the nodes to agree with their new version of the truth. This would be impossible, costly and time consuming.

Why are they called Miners?

Within the Bitcoin software is a limit of 21 million Bitcoins that can ever be produced. Much like when mining for physical gold, the precious metal only exists once it is brought to light from underground, so too with Bitcoin, it is only once the software rules are followed that any Bitcoin can be brought to light and realised.

What is the power behind a Bitcoin Miner?

The power behind a Bitcoin miner is its ability to solve the maths problem by following the Bitcoin software rules to validate transactions, create blocks and mine Bitcoin. The power is calculated in terahashes per second (TH/s) and at the moment one of the most popular Bitcoin miners, the Bitmain AntMiner S9j’s power is 14.5 TH/s.

How long do Bitcoin Miners last?

Older versions of the Antminer has been known to continue mining after five years. As technology improves I expect newer versions to mine a lot more efficiently so at some point it may be worth upgrading to the latest version.

Why does Bitcoin Mining become more difficult over time?

Historically money (£,$ etc) was backed by a weight in gold which gave it intrinsic value and helped regulated the market because there was a limited supply of gold in existence. Today nothing backs money and banks can simply print money whenever they want which devalues the money supply, increases prices and creates inflation.

To solve this problem, built into the Bitcoin software is a setting that means over time the difficulty for mining Bitcoin increases making it harder to solve blocks. Also the more miners there are competing on the network, the harder it is for blocks to be produced. Conversely if miners leave the market then mining becomes easier for the other miners as was seen in the 2018 bear market

To further regulate the supply of Bitcoin every four years the reward per block is halved. Back in 2008 when Bitcoin was conceived a desktop computer could mine a block and receive 50 Bitcoins.These days a lot more power is required using dedicated miners and the reward is 25 Bitcoins per block. Eventually the block reward halves many times and becomes so small that no new bitcoins can be created.

Creating scarcity in a market always increases the value of an item and historically after every “halving” the price per Bitcoin in monetary terms has increased. The next halving will be on May 21, 2020 so you may want to get involved before then so you don’t miss out on your mined Bitcoin potentially increasing in value.

How to Mine Bitcoin

There are three ways in which you can mine Bitcoin and deciding which method is best for you depends on your technical ability and budget. I am going to make the comparison of mining using a dedicated mining machine like the popular Bitmain AntMiner S9j which has 14.5 terahashes of power.

** PLEASE NOT THAT THE FIGURES BELOW ARE BASED AROUND MARKET CONDITIONS IN OCTOBER 2018 **

1. Home Mining

If you buy your own Bitmain AntMiner S9j you get a one year warranty meaning you may need to return it to Bitmain’s factory overseas or your local supplier if there are problems and wait for it to be repaired. The miner has four replaceable parts which means you could be mining for many years. Setting up a miner does require some technical expertise and an understanding of how to configure it properly.

A miner needs to be running 24/7 to ensure it can be mining all the time which means you need to have a cheap source of electricity and a cool environment.

Joining a mining pool is the only way to guarantee earning rewards as creating blocks on your own is impossible – once joined you will need to pay the pool anywhere between 1% and 3% in fees and the remainder is paid into your Bitcoin Wallet.

Its really difficult to work out the profitability of running your own miner as you don’t know how much maintenance, electricity costs, pool fees and downtime you will incur. An AntMiner S9j costs approximately $650 at the time of this guide so you would need to cover its cost in Mining revenue to start with.

Using the Bitmain Miner Calculator and assuming today’s Bitcoin price of $6,000, as an estimate, you could potentially be mining upto 0.0158 Bitcoin per month which equals $103. Then if you consider electricity costs of $126 ($0.14 per kwh) and a 3% pool fee, you may not even break even. Obviously if the Bitcoin price were to increase then you increase your chances of profitability.

2. Bitcoin Cloud Mining

Instead of mining at home there are mining farms (warehouses) full of miners. These farms called “Cloud Miners” like Genesis Mining in Iceland enable you to buy as much Bitcoin hashing power as you want in the form of a contract over a period of a few years. They run their own pools which reduce costs and any Bitcoin rewards you receive for mining with them is sent direct to your Bitcoin Wallet.

Using Genesis Mining as an example, currently their cost for 15 terahashes of power (0.5 terahashes more than an Bitmain AntMiner S9j) is $4200 for a five year contract which you pay upfront and works out to be $280 per terahash. They also deduct a daily maintenance fee of £1.96 from any Bitcoin payouts you mine which works out to £3577 for the five year period.

Link to Genesis Mining Pricing

My experience of these type of contracts is that they only pay out when Bitcoin is profitable (i.e. the price against the US Dollar is high) and the price per Bitcoin covers the cost of the mining machine’s costs. In a positive market mining Bitcoin can be very profitable, however in a negative market it can be difficult to cover mining costs so you could end up at a loss over the period of the contract. It was possible to mine 0.01 Bitcoin when Bitcoin was priced at $15,000 in 2017 and nothing when it was priced at $6,000 the following year, so really difficult to estimate the total Bitcoin payout over five years.

3. Bitcoin Mining as a Service (MAAS)

A newer way to mine Bitcoin is to buy your own AntMiner S9j through a mining farm outright and let them install it, take care of the maintenance and send the Bitcoin your miner outputs automatically to your Bitcoin wallet. This type of mining is called “Mining as a Service” (MAAS).

The Bitcoin mining company Elevate Group has a farm based in Siberia which has an average temperature of -2c degrees (ideal for cooling the miners) and really low fuel costs ($0.055 per kilowatt hour). They also run their own mining pool which means unlike public ones there are no pool fees to pass on to you the miner.

Their farm is located in the same town as Bitmain the company that manufactures the AntMiner S9j which means downtime is limited to a few days if repairs are required and they will continue to maintain the miners beyond the official warranty period of one year without extra fees. Their costs are $70 per terahash ($280 with Genesis Mining) and you pay a 20% maintenance fee which is taken off your Bitcoin Payouts paid monthly.

The main benefit of doing Bitcoin Mining as a Service (MAAS) is that regardless as to the market price of Bitcoin, you will always be mining a certain amount. For example if you bought one miner with the Elevate Group costing $1,199 paid upfront and including all lifetime maintenance and repair costs, you could potentially receive an average payout of 0.007 Bitcoin ($45) per month depending on mining difficulty while one Bitcoin is priced at $6,000. If Bitcoin were to double in value against the US dollar then the payouts would be worth $90 per month. Assuming Bitcoin where to stay at $6,000 then I estimate your miner with Elevate could break even after 26 months. Should Bitcoin’s price reach $12,000 then you cover the miner’s cost in 14 months. The miner is paid for and of course AntMiners have been known to continue mining for upto five years.

How does Bitcoin mining affect the environment?

Its true that Bitcoin mining consumes a lot of electricity, however what the mainstream media doesn’t focus on is the energy used to produce that electricity. Most Bitcoin farms are located in areas that require minimal cooling like the Elevate farm in cold Siberia or are using renewable energy sources like Genesis Mining facility in Iceland powered by geothermal energy.

What’s also ignored is the cost to maintain our current monetary system. There are numerous factors to take into account including water, paper, gasoline, electricity to mine the metals, the energy for destroying and transporting physical money; heating, water, garbage disposal, cleaning for the offices full of employees, the energy needed to power all the ATMs and the computers to perform transactions. It is estimated that our old monetary system consumes 70 terawatts of electricity per year compared to Bitcoin’s 30 terawatts!

How profitable is it to mine Bitcoin?

This really does depend on the market price of Bitcoin and how low you can keep the operational costs by reducing maintenance downtime, pool fees and electricity costs.

Is it too late to get involved in Bitcoin Mining?

When I consider the amount of resources that are being pumped into Bitcoin mining farms it demonstrates that Bitcoin is not going away and in fact the opposite, more and more companies and individuals are investing in Bitcoin miners and creating wealth for themselves and investing in the new monetary system. My belief is it isn’t too late, however naturally you have to do your own cost/benefit analysis for your own personal circumstances before making a commitment.

How I can help you?

My background is in technology and training and for over 10 years I have provided IT Support to home and small business users through my IT company ithound.co.uk. In recent years I have added Cryptocurrencies to my product offering with cryptohound.me.

Whether you are a business wanting to accept cryptocurrencies or an individual interested in investing in them, I will help you get started and provide training and support to give you confidence using them.

I regularly write blogs both on my website and the Steemit platform so be sure to connect with me there. If you would like to support my work please check out my affiliate links below which help finance my work:

- Mine Bitcoin and earn passive income with the Elevate Group

- Earn $10 worth of free Bitcoin on your first trade with Coinbase

- Buy Bitcoin and Cryptocurrencies using the Binance Exchange

- Protect your Cryptocurrencies with a Ledger Hardware wallet

Carl Hughes, The Crypto Hound

Signal Messenger: +447919 562 418

Telegram: @ flowingman

cryptohound.me | @Steemit | @Minds | @Twitter | @LinkedIn | @Trybe | @Gab

Recent Comments